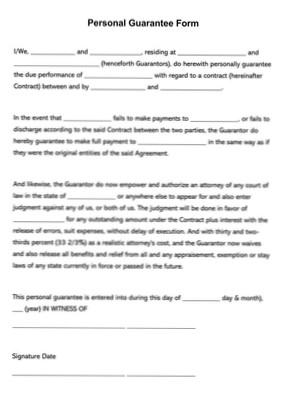

When a personal guarantee is given, the principals of the company pledge their own assets and agree to repay a debt from personal capital in case the company defaults. In short, the business owner or principal becomes a cosigner on the credit application.

A guaranteed loan is used by borrowers with poor credit or little in the way of financial resources; it enables financially unattractive candidates to qualify for a loan and assures that the lender won't lose money. Guaranteed mortgages, federal student loans, and payday loans are all examples of guaranteed loans.

A personal guaranty is not enforceable without consideration

In fact, no contract is enforceable without consideration. A personal guaranty is a type of contract. A contract is an enforceable promise. The enforceability of a contract comes from one party's giving of “consideration” to the other party.

The easiest banks to get a personal loan from are USAA and Wells Fargo. USAA does not disclose a minimum credit score requirement, but their website indicates that they consider people with scores below the fair credit range (below 640). So even people with bad credit may be able to qualify.

Yes, you are personally liable for your SBA loan. ... This means that if the business fails to repay the loan, the lender can pursue your personal assets.

Use Caution When Taking on Loans

A loan guarantee is a contractual obligation between the government, private creditors and a borrower—such as banks and other commercial loan institutions—that the Federal government will cover the borrower's debt obligation in the event that the borrower defaults.

Conventional loans are not insured by a government agency, so they're riskier for lenders and tend to have stricter eligibility requirements. Government-backed loans have different cost structures, including upfront fees and mortgage insurance requirements.

Quicken Loans today is the F.H.A. insurance program's largest participant.

Unless a business is a sole proprietorship, personal guarantees can only be discharged by filing an individual bankruptcy. A business bankruptcy will not eliminate a personal guarantee. Likewise, the Chapter 13 co-debtor stay only applies to consumer debts and personal guarantees are usually considered business debts.

In most states a personal guarantee is deemed a written contract under their statutes and case law. As such, the statute of limitations for breach of a written contract varies state by state, but typically it is a four (4) year statute of limitations.

What happens if you default on a personal guarantee? Defaulting on a loan when you've signed a personal guarantee will likely impact your credit score for up to 10 years. If you default and you haven't signed a personal guarantee, your business's credit score will be impacted.

Yet No Comments