Trusts can help sidestep inheritance tax By writing a life-insurance policy in trust, the proceeds from the policy can be paid directly to the beneficiaries rather than to your legal estate, and will therefore not be taken into account when inheritance tax is calculated.

Life Insurance Beneficiaries

In most cases, it makes better sense to name your beneficiaries individually on life insurance policies versus naming a trust as beneficiary. ... Trusts are not considered individuals; therefore, life insurance proceeds paid to trusts are generally subjected to estate tax.

Putting your life insurance policy in trust involves a legal arrangement that helps to ensure that the money from that policy is used exactly as you intended, regardless of the value of your estate. ... It also means that your beneficiaries will receive the money much quicker, whether a will has been written or not.

To put your life insurance into a trust, you'll need to select trustees, find an insurance provider, and decide on whether you want to place life insurance into the trust immediately or assign it to the trust at a later date.

The cost to set up irrevocable trusts through a major law firm runs between $2,000 and $5,000, primarily because the permanency of such a trust and the amount of upfront work and thought that must go into getting it right the first time.

The only real restriction is for minors, as you would need to designate a trust or legal guardian as the beneficiary to provide them the death benefit. While you can name anyone as a beneficiary, just make sure to notify them and provide them with a copy of your life insurance policy.

Drawbacks of a Living Trust

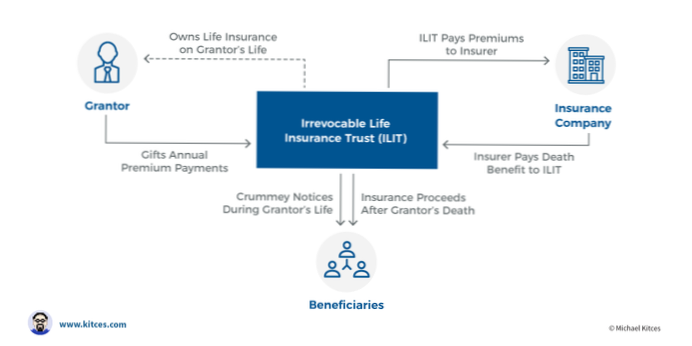

The insurance trust owns your life insurance policy. The trust holds the insurance policy with you as the named insured and when you die, the insurance benefit is paid to the trust.

To protect the insurance proceeds from this, you can write the policy into a trust. The trust ensures that the proceeds of the mortgage life insurance go to the Person Insured's intended beneficiaries. ... With the trust, the insurance proceeds will be paid more quickly and directly to the lender.

Some states, by statue or case law, hold that only the beneficiary named in the beneficiary designation form is entitled to these assets, regardless of whether your will, trust or other document specifically identifies the account and names someone else as its beneficiary.

Can a beneficiary be a trustee for a life insurance trust? You may wish to place your life insurance policy in a trust and appoint either a legal professional or trusted friend/family member to disburse the proceeds according to your wishes.

A settlor or trustee can also be a beneficiary of same trust. ... The trustee may be a person or an entity such as a company (typically when management fees are charged). The settlor may appoint multiple trustees. Although the trustees of a trust may change, a trust must always have at least one trustee.

Yet No Comments